section summary:

- an investment asset's performance and risk characteristics can be determined via a CAPM plot

- the beta (risk) can be minimized by adding low beta assets (e.g. utility stocks) and/or negative beta assets (e.g. gold or short-position assets) to a portfolio

- at Prime Cognos, our software and services compose portfolios that minimize beta and thus reduce the risk associated with the portfolios

The theoretical rate of return for an investment is governed by the capital asset pricing model (CAPM).

CAPM is defined as:

where:

- Ri is the expected return of the investment asset

- Rm is the expected return of the market

- βi (the beta) is the sensitivity of the expected return of the investment asset to the expected return to the market

- αi (the alpha) is the active return of investment asset (i.e. the performance of that investment)

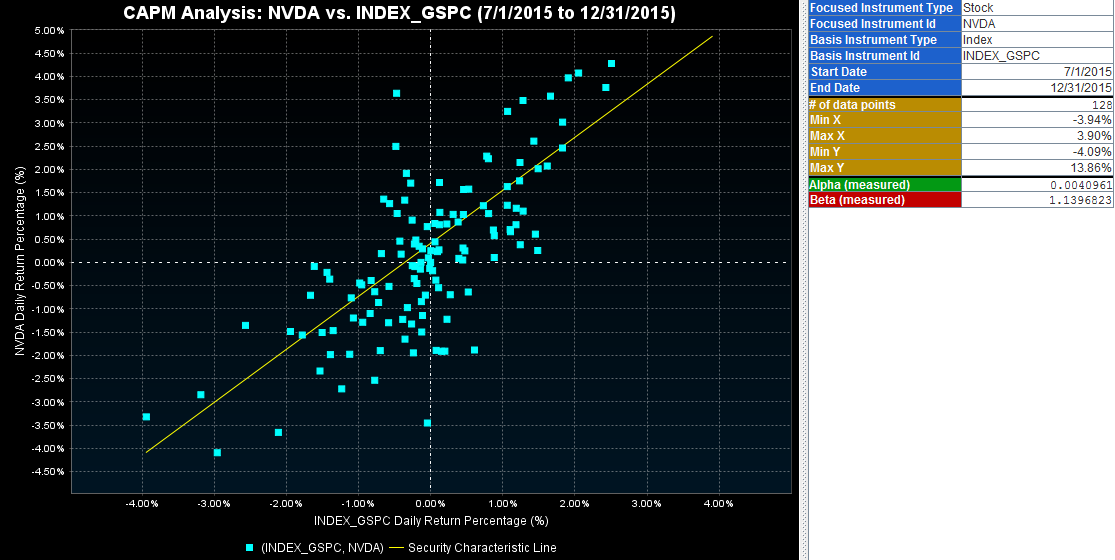

The values for alpha and beta can be seen visually by plotting the daily returns of the investment asset against the daily returns of the market index. For example the below scatter plot shows the daily returns of NVIDIA Corporation (NVDA) versus the S&P 500 index (INDEX_GSPC) for the six months between 7/1/2015 and 12/31/2015:

A yellow line (known as the Security Characteristic Line (SCL)) is placed through the scatter plot by performing a linear regression. The beta of the investment (NVDA in this case) is measured as the slope of the SCL. In general, a beta of less than 1 indicates that the investment is less volatile than the market, while a beta of more than 1 indicates that the investment is more volatile than the market. The alpha of the investment is measured as the y-intercept of the SCL. Non-zero values of alpha indicate returns of the investments not associated with market.

In comparison to individual investments, the CAPM formula for a portfolio is mostly the same except that weights are given to each constituent asset:

Thus the expected return for a portfolio is the sum of the weight adjusted return of each investment. Similarly the beta of the portfolio is the sum of the weight adjusted beta of each investment:

In composing a portfolio, market risk (βpRm) can be minimized by reducing the beta of the portfolio (βp). This is accomplished by adding low beta assets (e.g. utility stocks) and/or negative beta assets (e.g. gold or short-position assets) to a portfolio.

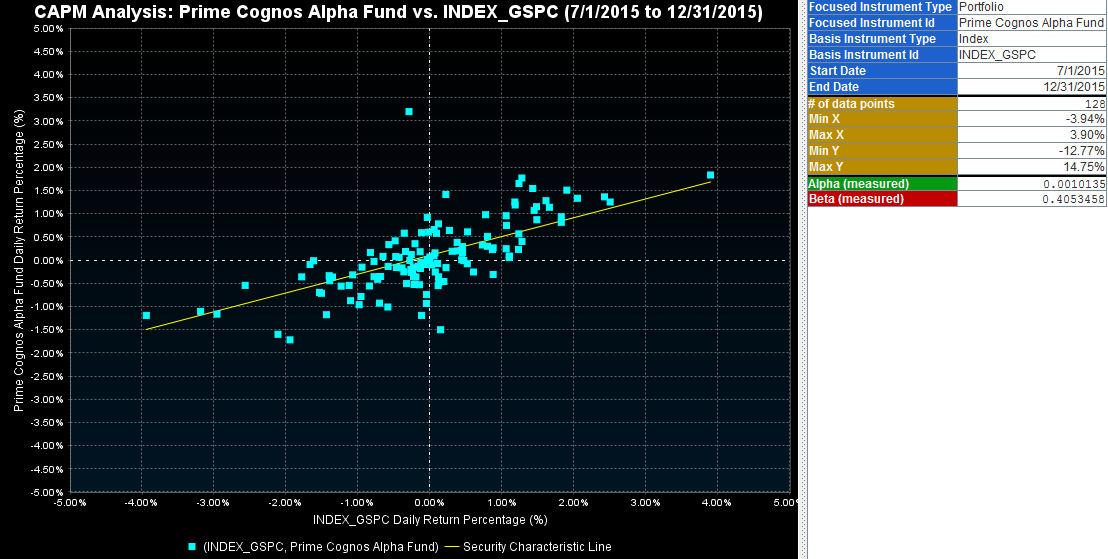

When this is done you will see a scatter plot and Security Characteristic Line like the following:

Notice how the dots are more closely bunched and slope of the SCL is flatter. This corresponds to the lower beta of the portfolio. If the beta is managed all the way to zero the portfolio is said to be market neutral, meaning the portfolio's return is not affected by the market, but rather only by it's alpha (the active return of it's investments).

At Prime Cognos, our software and services compose portfolios that minimize beta and thus reduce the market risk associated with the portfolios.